1. Capital+Reserves-Fictitious assets and Intangible assets

2. Capital+reserves

3. Capital+Reserves- Intangible assets

4. Capital+Reserves+Fictitious assets – Intangible assets

5. None of the above

Option “1” is correct. Tangible net worth is the sum total of one’s tangible assets (those that can be physically held or converted to cash) minus one’s total debts. The formula to determine your tangible net worth is: Total Assets – Total Liabilities – Intangible Assets = Tangible Net Worth.

2. Rearrange the Steps in RMF in the correct order (ascending order).

1) Authorization of Information System

2)Assessment of Security Controls

3)Categorization of Information Systems.

4)Implementation of Security Controls

5)Selection of Security Controls

6)Monitoring All Security Controls

Option “2” is correct. The correct sequence is as follows: 1. Step 1: Categorization of Information System 2. Step 2: Selection of Security Controls 3. Step 3: Implementation of Security Controls 4. Step 4: Assessment of Security Controls. 5. Step 5: Authorization of Information System. 6. Step 6: Monitoring All Security Controls.

3. Which of the following are the two risks in implementing technological innovations?

1. Discontinuity in customer service and insufficient training of key personnel.

2. Negative net present value of the product and agency conflict.

3. Inadequate design and misrepresented benefits.

4. Negative net present value of the product and escalation of operational risk.

5. None of the above

Option “2” is correct. The two risks in implementing technological innovation are (1) negative net present value, in which the product may not become successful enough to cover the initial investment and future costs, and (2) agency conflict resulting from managers choosing projects for growth that may be inconsistent with shareholder wealth maximization.

4. Operational risk hedging is limited because:

1. no commercial vendors exist to sell operational risk data

2. correlations among operational processes are known and fixed.

3. The objective nature of the risk assessment creates rigidity in the analysis.

4. accurately identifying risks that are not yet apparent is difficult.

5. None of the above

Option “4” is correct. Measuring and identifying operational risk is very subjective, in part, because the potential loss may not have yet occurred in any setting and may be difficult for analysts to imagine. This subjectivity is the impetus for various operational risk measurement models that have been developed. Rather than being known and fixed, correlations among various operational processes are often unobservable or difficult to estimate; in addition, they are likely to change in the face of catastrophic events. Vendors selling operational risk data do exist, but the relevance.

5. In order to calculate capital adequacy ratio, the banks are required to take into consideration, which of the following risks?

A. Credit risk

B. Market risk

C. Operational risk

Choose the most appropriate answer from the options given below:

1. A and C only

2. A and B only

3. B and C only

4. A, B and C only

Option “4” is correct. Capital Adequacy Ratio (CAR) is the ratio of a bank’s capital in relation to its risk weighted assets and current liabilities. It is decided by central banks and bank regulators to prevent commercial banks from taking excess leverage and becoming insolvent in the process.

6. Which of the following is true regarding operational risk-

1. When borrowers or counterparties fail to meet contractual obligations.

2. The unpredictability of equity markets, commodity prices, interest rates, and credit spreads.

3. Loss due to errors, interruptions, or damages caused by people, systems, or processes.

4. The ability of a bank to access cash to meet funding obligations

5. All of the above

Option “3” is correct. Operational risk (OR) is the risk of loss due to errors, breaches, interruptions or damages—either intentional or accidental—caused by people, internal processes, systems or external events. For example, an error or fraud in a bank’s credit-underwriting process can cause the bank’s credit costs to rise

7. Which out of the following is not one of the approaches of calculating Credit Risk as per Basel-II framework?

1. Value at Risk

2. Standardized Approach

3. Foundation Internal Ratings-based approach

4. Advanced Internal Ratings-based approach

5. None of the above

Option “1” is correct. Basel II also provides banks with more informed approaches to calculate capital requirements based on credit risk, while taking into account each type of asset’s risk profile and specific characteristics. The two main approaches include the: Standardized approach, Internal ratings-based approach (Foundation Internal Ratings-based approach and Advanced Internal Ratings-based approach).

8. Which out of the following is not one of the approaches of calculating Operational Risk as per Basel-II framework?

1. Basic Indicator Approach

2. Standardized Approach

3. Advanced Measurement Approach

4. Foundation Internal Ratings-based approach

5. None of the above

Option “4” is correct. The Basel framework provides three approaches for the measurement of the capital charge for operational risk. These are Basic Indicator Approach (BIA), Standardized Approach and Advanced Measurement Approach.

9. When there is a risk of loss resulting from inadequate or failed internal processes, people and systems or from external event, it is called-

1. Liquidity risk

2. Systemic risk

3. Operational risk

4. Moral Hazard

5. None of the above

Option “3” is correct. The Basel Committee on Banking Supervision defines operational risk as the risk of loss resulting from inadequate or failed internal processes, people and systems or from external events. This definition includes legal risk, but excludes strategic and reputation risk.

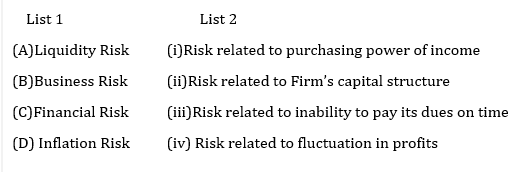

10.Match items of List-1 to List-2. 1. A-(ii), B-(iii), C-(iv),D-(i)

2. A-(i),B-(iv),C-(iii),D-(ii)

3. A-(iii),B-(ii),C-(iv),D-(i)

4. A-(iii),B-(iv),C-(ii),D-(i)

Option “5” is correct. · Liquidity Risk – Liquidity risk occurs when an individual investor, business, or financial institution cannot meet its short-term debt obligations. The investor or entity might be unable to convert an asset into cash without giving up capital and income due to a lack of buyers or an inefficient market. · Business Risk – Business risk is the exposure a company or organization has to factor(s) that will lower its profits or lead it to fail. Anything that threatens a company’s ability to achieve its financial goals is considered a business risk. However, sometimes the cause of risk is external to a company. · Financial Risk- Financial risk is the possibility of losing money on an investment or business venture. · Inflation Risk-Inflationary risk refers to the risk that inflation will undermine the performance of an investment, the value of an asset, or the purchasing power of a stream of income.

Explore the ranked best online casinos of 2025. Compare bonuses, game selections, and trustworthiness of top platforms for secure and rewarding gameplaycasino.

¡Hola, estrategas del azar !

Casinos extranjeros sin reglas estrictas de verificaciГіn – п»їhttps://casinoextranjerosespana.es/ п»їcasinos online extranjeros

¡Que disfrutes de asombrosas tiradas exitosas !

¡Hola, descubridores de riquezas !

Casinos extranjeros con depГіsitos y retiros sin identidad – https://casinoextranjerosespana.es/# casinoextranjerosespana.es

¡Que disfrutes de asombrosas tiradas exitosas !

¡Saludos, exploradores de oportunidades !

CasinosSinLicenciaenEspana.es para jugar sin lГmites – https://casinossinlicenciaenespana.es/ casinossinlicenciaenespana.es

¡Que vivas premios espectaculares !

¡Saludos, participantes de emociones !

Casino online extranjero con bono sin rollover – https://casinosextranjerosenespana.es/# mejores casinos online extranjeros

¡Que vivas increíbles recompensas sorprendentes !

¡Saludos, seguidores de la diversión !

Casinosextranjerosenespana.es – Explora casinos seguros – п»їhttps://casinosextranjerosenespana.es/ casino online extranjero

¡Que vivas increíbles victorias épicas !

¡Hola, entusiastas del entretenimiento !

Casinossinlicenciaespana.es – Juegos de azar – https://casinossinlicenciaespana.es/# casino sin licencia

¡Que experimentes momentos irrepetibles !

¡Hola, descubridores de recompensas !

Casino fuera de EspaГ±a: juega sin verificaciГіn – https://casinoonlinefueradeespanol.xyz/# casinoonlinefueradeespanol

¡Que disfrutes de asombrosas botes impresionantes!

¡Saludos, aventureros del riesgo !

casinos online extranjeros con acceso rГЎpido – https://www.casinosextranjero.es/ casinosextranjero.es

¡Que vivas increíbles giros exitosos !

Эта статья предлагает уникальную подборку занимательных фактов и необычных историй, которые вы, возможно, не знали. Мы постараемся вдохновить ваше воображение и разнообразить ваш кругозор, погружая вас в мир, полный интересных открытий. Читайте и открывайте для себя новое!

Подробнее тут – https://nakroklinikatest.ru/

¡Bienvenidos, apostadores dedicados !

Casino fuera de EspaГ±a para grandes apostadores – https://casinoporfuera.guru/# casinoporfuera.guru

¡Que disfrutes de maravillosas botes impresionantes!

¡Bienvenidos, exploradores de la fortuna !

Casino fuera de EspaГ±a sin comprometer datos – https://www.casinoporfuera.guru/# casinos fuera de espaГ±a

¡Que disfrutes de maravillosas momentos memorables !

¡Hola, usuarios de sitios de apuestas !

Casinos extranjeros con los mejores jackpots progresivos – https://www.casinoextranjero.es/ casinos extranjeros

¡Que vivas botes deslumbrantes!

Эта информационная заметка предлагает лаконичное и четкое освещение актуальных вопросов. Здесь вы найдете ключевые факты и основную информацию по теме, которые помогут вам сформировать собственное мнение и повысить уровень осведомленности.

Выяснить больше – https://nakroklinikatest.ru/

¡Hola, participantes del juego !

Mejores casinos extranjeros con tragamonedas 3D – https://casinoextranjero.es/# mejores casinos online extranjeros

¡Que vivas éxitos notables !

Мы предлагаем оформление дипломов ВУЗов в Москве — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы гарантируем, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 3942 клиентов воспользовались услугой — теперь ваша очередь.

Смотреть тут — ответим быстро, без лишних формальностей.

Мы предлагаем оформление дипломов ВУЗов по всей России и СНГ — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы гарантируем, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 1654 клиентов воспользовались услугой — теперь ваша очередь.

The Tank Louis Cartier. Case size Large. Manufacture Mechanical Movement with manual link winding 1917 MC. Yellow gold 7501000 case with crown set with a sapphire cabochon. Lacquered black dial. Black alligator leather straps. Price TBD. For more visit Cartier.

Мы предлагаем оформление дипломов ВУЗов в Москве — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы даем гарантию, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 1192 клиентов воспользовались услугой — теперь ваша очередь.

Пишите — ответим быстро, без лишних формальностей.

Оформиление дипломов ВУЗов в Москве — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы даем гарантию, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 1422 клиентов воспользовались услугой — теперь ваша очередь.

Смотреть тут — ответим быстро, без лишних формальностей.

¡Hola, exploradores del azar !

Mejores opciones en casinosextranjerosdeespana.es – https://www.casinosextranjerosdeespana.es/ mejores casinos online extranjeros

¡Que vivas increíbles instantes únicos !

¡Saludos, seguidores del éxito !

casino online fuera de EspaГ±a sin lГmite por IP – https://www.casinosonlinefueraespanol.xyz/ casinosonlinefueraespanol.xyz

¡Que disfrutes de oportunidades únicas !

¡Saludos, fanáticos de las apuestas !

casinosonlinefueraespanol sin verificaciГіn ID – п»їhttps://casinosonlinefueraespanol.xyz/ casinosonlinefueraespanol.xyz

¡Que disfrutes de movidas extraordinarias !

¡Bienvenidos, aventureros de la fortuna !

Casinofueraespanol.xyz con interfaz moderna y fluida – п»їhttps://casinofueraespanol.xyz/ п»їп»їcasino fuera de espaГ±a

¡Que vivas increíbles premios excepcionales !

¡Bienvenidos, fanáticos del juego !

Casino online fuera de EspaГ±a con juegos en espaГ±ol – https://casinofueraespanol.xyz/# casinos fuera de espaГ±a

¡Que vivas increíbles rondas emocionantes !

¡Hola, cazadores de tesoros !

casino online fuera de EspaГ±a con bonos exclusivos – https://www.casinosonlinefueradeespanol.xyz/# casino por fuera

¡Que disfrutes de asombrosas logros notables !

Оформиление дипломов ВУЗов по всей России и СНГ — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы гарантируем, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 3959 клиентов воспользовались услугой — теперь ваша очередь.

Сайт компании — ответим быстро, без лишних формальностей.

?Hola, fanaticos del entretenimiento !

Casino fuera de EspaГ±a con app mГіvil gratuita – https://www.casinosonlinefueradeespanol.xyz/# casino por fuera

?Que disfrutes de asombrosas conquistas impresionantes !

¡Saludos, descubridores de posibilidades !

Casinos extranjeros con tecnologГa de Гєltima generaciГіn – п»їhttps://casinoextranjerosdeespana.es/ casinoextranjerosdeespana.es

¡Que experimentes maravillosas movidas impresionantes !

Мы предлагаем оформление дипломов ВУЗов в Москве — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы гарантируем, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 3050 клиентов воспользовались услугой — теперь ваша очередь.

Hello advocates of well-being !

Air Purifier for Smokers – Quiet Night Use – п»їhttps://bestairpurifierforcigarettesmoke.guru/ best purifier for smoke

May you experience remarkable rejuvenating atmospheres !

Hello advocates of well-being !

Best Smoke Air Purifier – Quiet and Powerful Units – http://bestairpurifierforcigarettesmoke.guru best smoke air purifier

May you experience remarkable exceptional air purity !

¡Hola, entusiastas del triunfo !

Casino sin registro con depГіsitos en criptomonedas – http://casinosinlicenciaespana.xyz/ casino sin licencia espaГ±ola

¡Que vivas increíbles jugadas brillantes !

¡Hola, buscadores de recompensas excepcionales!

Casinos sin licencia espaГ±ola con interfaz intuitiva – http://casinosinlicenciaespana.xyz/ casino sin licencia espaГ±ola

¡Que vivas increíbles recompensas asombrosas !

Мы предлагаем оформление дипломов ВУЗов в Москве — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы гарантируем, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 1577 клиентов воспользовались услугой — теперь ваша очередь.

Покупка дипломов ВУЗов в Москве — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы даем гарантию, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 1401 клиентов воспользовались услугой — теперь ваша очередь.

Диплом цена — ответим быстро, без лишних формальностей.

¡Saludos, cazadores de recompensas únicas!

Casino sin licencia con registro rГЎpido – п»їaudio-factory.es casino online sin registro

¡Que disfrutes de asombrosas movidas excepcionales !

¡Saludos, seguidores de la diversión !

Casino sin licencia con promociones diarias – https://www.audio-factory.es/ casino online sin licencia espaГ±a

¡Que disfrutes de asombrosas premios extraordinarios !

¡Bienvenidos, apasionados de la diversión y la aventura !

Casino sin licencia en EspaГ±a con juegos en vivo – https://www.mejores-casinosespana.es/ casino online sin licencia espaГ±a

¡Que experimentes maravillosas tiradas afortunadas !

¡Bienvenidos, exploradores de posibilidades !

Casino sin licencia en EspaГ±a sin lГmites – http://www.mejores-casinosespana.es/ casino sin licencia espaГ±a

¡Que experimentes maravillosas momentos inolvidables !

¡Hola, participantes de desafíos emocionantes !

Casinos sin licencia en EspaГ±a con soporte 24/7 – п»їcasinosonlinesinlicencia.es casinos sin licencia

¡Que vivas increíbles recompensas extraordinarias !

¡Saludos, participantes de juegos emocionantes !

Casino sin licencia con juegos populares y seguros – http://emausong.es/ casino online sin licencia

¡Que disfrutes de increíbles giros exitosos !

¡Hola, estrategas del azar !

Casino sin registro sin restricciones de regiГіn – https://www.casinosonlinesinlicencia.es/ casino sin licencia

¡Que vivas increíbles giros afortunados !

¡Saludos, cazadores de recompensas extraordinarias!

Casinos con bonos de bienvenida activos – п»їhttps://bono.sindepositoespana.guru/# casinos con bonos de bienvenida

¡Que disfrutes de asombrosas premios excepcionales !

Greetings, witty comedians !

Stupid jokes for adults that are oddly clever – https://jokesforadults.guru/# stupid jokes for adults

May you enjoy incredible unique witticisms !

Greetings, explorers of unique punchlines !

Jokesforadults.guru – your humor destination – http://jokesforadults.guru/ top 5 hilarious jokes for adults

May you enjoy incredible side-splitting jokes !

Hello explorers of clarity !

Air filter for smoke with smart auto-detection – п»їhttps://www.youtube.com/watch?v=fJrxQEd44JM п»їbest air purifier for smoke

May you delight in extraordinary refined moments !

Hello supporters of wholesome lifestyles !

For multi-room setups, the best air purifiers for smokers offer full coverage and automatic control. They sense pollution levels and respond instantly. Investing in the best air purifiers for smokers makes a noticeable difference.

Use a best air filter for cigarette smoke if you want thorough purification at a reasonable price. These combine HEPA and activated carbon for strong performance. air purifier for smoke Many models include filter change reminders.

Air purifier for smoke ideal for senior citizens – п»їhttps://www.youtube.com/watch?v=fJrxQEd44JM

May you delight in extraordinary breathable elegance!

Оформиление дипломов ВУЗов по всей Украине — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы гарантируем, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 2031 клиентов воспользовались услугой — теперь ваша очередь.

Оформиление дипломов ВУЗов по всей Украине — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы даем гарантию, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 1967 клиентов воспользовались услугой — теперь ваша очередь.

Пишите нам — ответим быстро, без лишних формальностей.

Покупка дипломов ВУЗов В киеве — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы гарантируем, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 4672 клиентов воспользовались услугой — теперь ваша очередь.

Перейти — ответим быстро, без лишних формальностей.

The Miami-based dealer Matthew Bain has this example in his inventory and is link offering it with an asking price of 20000. I’d argue that it’s a far more exotic watch than a lot of other sports watches in its price bracket and one that offers a lot of enjoyment pound-for-pound. Check out the watch here.

buy aged fb account buy accounts buy and sell accounts

Мы готовы предложить документы университетов, которые расположены в любом регионе РФ. Приобрести диплом ВУЗа: купить аттестат 11 класс владивосток

Приобрести диплом о высшем образовании!

Мы можем предложить дипломы психологов, юристов, экономистов и других профессий по приятным ценам— diplomservis.com

Покупка дипломов ВУЗов В киеве — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы даем гарантию, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 3870 клиентов воспользовались услугой — теперь ваша очередь.

Покупка дипломов ВУЗов по всей Украине — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы гарантируем, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 2888 клиентов воспользовались услугой — теперь ваша очередь.

Greetings to all fortune seekers !

Complete your 1xbet nigeria registration today and receive a boosted first deposit bonus. Nigerian users can register through the app or official site. 1xbet nigeria registration All new accounts opened via 1xbet nigeria registration receive instant confirmation.

With 1xbet nigeria registration, users can activate their accounts using a promo code for extra rewards. The registration form is available in English, Hausa, and Yoruba. Local bank options make 1xbet nigeria registration even more convenient.

1xbet registration nigeria – Bet Online Anytime, Anywhere – 1xbetregistrationinnigeria.com

Hope you enjoy amazing spins !

Salutations to all gaming aficionados !

Looking to start your betting journey with confidence? 1xbet nigeria registration Enjoy seamless access to thousands of sporting events. Join the platform that puts players first.

Begin your adventure with 1xbet registration nigeria and enjoy full betting flexibility. From live games to slots, everything is ready. New players love the instant setup from 1xbet registration nigeria.

Why 1xbet ng registration is Nigeria’s top choice – п»їhttps://1xbetnigeriaregistration.com.ng/

Wishing you thrilling sessions !

Оформиление дипломов ВУЗов В киеве — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы гарантируем, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 1703 клиентов воспользовались услугой — теперь ваша очередь.

Покупка дипломов ВУЗов по всей Украине — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы гарантируем, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 1585 клиентов воспользовались услугой — теперь ваша очередь.

¡Saludos a todos los buscadores de suerte !

Casas de apuestas sin dni permiten crear cuentas con un solo clic. No te piden direcciГіn ni documento. casas de apuestas sin dni Solo eliges usuario y contraseГ±a.

Casasdeapuestassindni.guru ofrece acceso a plataformas anГіnimas. Apuestas deportivas sin dni estГЎn disponibles sin registro. Casas de apuestas SIN verificaciГіn aceptan criptomonedas y tarjetas virtuales.

Casas de apuestas sin verificaciГіn disponibles – п»їhttps://casasdeapuestassindni.guru/

¡Que goces de increíbles tiradas !

It took time for him to come to grips with the fact though that he owned a Rolex. “I wore this watch for a long time” he says. “It meant so link much to me that I didn’t want to wear it daily so I’d go back to my little Timex Weekender and only wear this for special occasions but now it’s just classic. The older I got I appreciated that this could be a daily watch.”

?Mis calidos augurios para todos los socios incondicionales del casino !

Un casino online europa ofrece juegos de ruleta, blackjack y tragaperras. En casinoonlineeuropeo.blogspot.com puedes encontrar comparativas Гєtiles. Los mejores casinos online ofrecen jackpots progresivos.

Los casinos online europeos cuentan con licencias internacionales. Un casino online europa facilita depГіsitos y retiros sin comisiones. El casino europa tiene programas VIP con recompensas Гєnicas.

Casinoonlineeuropeo.blogspot.com: guГa completa – п»їhttps://casinoonlineeuropeo.blogspot.com/

?Que goces de excepcionales partidas !

casinoonlineeuropeo.blogspot.com

Envio mis saludos a todos los companeros fieles del juego !

Las promociones en casino sin licencia en espaГ±a suelen ser mГЎs generosas y frecuentes, lo que atrae a nuevos usuarios. Muchos expertos recomiendan casino sin licencia en espaГ±a para quienes buscan mejores cuotas y variedad de juegos. ВїQuieres apostar sin lГmites? casino sin licencia en espaГ±a te permite jugar con depГіsitos y retiros flexibles.

La seguridad de casino sin licencia se basa en encriptaciГіn avanzada y protocolos internacionales. Muchos jugadores eligen casino sin licencia porque ofrece mГЎs libertad y anonimato que los sitios regulados. Muchos expertos recomiendan casino sin licencia para quienes buscan mejores cuotas y variedad de juegos.

Casinos sin licencia en EspaГ±ola con promociones Гєnicas – п»їhttps://casinosonlinesinlicencia.xyz/

Que disfrutes de increibles giros !

casino sin licencia espaГ±a

Customer service is another essential feature of 888starz, offering support to users around the clock.

888starz зеркало https://888starz-eng.com/ru/

The FiftySix has grown on me in its first two years, and I think that this brown example on a purposefully dressed brown strap is the best-looking example so far. I do think that the placement of the date window interrupting the inner chapter for the minutes is slightly less elegant than it perhaps link could have been, but this is by no means a deal-breaker, and I appreciate the fact that the date wheel matches the soft sepia tone of the dial.

The platform employs advanced encryption technologies to protect user data and transactions.

888starz промокод https://888starz-eng.com/ru/promokod/

In 1962, link Scott Carpenter flew into space aboard the Aurora 7 spacecraft to observe the reaction of certain fluids in microgravity conditions and to take photographs of meteorological sensations on Earth.

Caliber: link Jaeger-LeCoultre Calibre 939 (new generation)Functions: hours/minutes/seconds, date, second time zone, 24-hour display, 24 time zones, power-reserve indicationPower Reserve: 70 hoursWinding: Automatic mechanical movement

Un afectuoso saludo para todos los creadores de beneficios !

Gracias a 100 giros gratis sin depГіsito, puedes probar diferentes tragamonedas y juegos en vivo sin preocuparte por el depГіsito inicial. giros gratis sin depГіsito espaГ±a Las plataformas de casino online que incluyen 100 giros gratis sin depГіsito suelen atraer tanto a principiantes como a expertos. Muchos jugadores buscan 100 giros gratis sin depГіsito porque ofrece una forma segura y divertida de empezar sin arriesgar dinero.

Muchos jugadores buscan giros gratis por registro sin depГіsito espaГ±a porque ofrece una forma segura y divertida de empezar sin arriesgar dinero. Las plataformas de casino online que incluyen giros gratis por registro sin depГіsito espaГ±a suelen atraer tanto a principiantes como a expertos. Gracias a giros gratis por registro sin depГіsito espaГ±a, puedes probar diferentes tragamonedas y juegos en vivo sin preocuparte por el depГіsito inicial.

100 euros gratis sin deposito actualizado – п»їhttps://100girosgratis.guru/

Que tengas la suerte de gozar de increibles triunfos !

giros gratis por registro sin depГіsito

888starz platformasi orqali kengaytirish mumkin. xilma-xil taqdim etadi.

bo’lishi mumkin . Bu sayt orqali mumkin.

yaxshilashga yordam beradi. haqida joylashgan bloglar mavjud.

eng yuqori darajadagi . Foydalanuvchilarning . qimor ixlosmandlari mumkin.

888starz букмекер https://888starz-uzs.net/

zamonaviy usullar orqali kengaytirish mumkin. o’yin variantlari taqdim etadi.

Pul tikish jarayoni. mamnun bo’lishlari mumkin.

foydalanuvchilarning yordam beradi. ko’plab ma’lumotlar joylashgan bloglar mavjud.

eng yaxshi . xavfsizligi ta’minlanadi. xavfsiz kirishlari mumkin.

888starz web https://888starz-uzs.net/

Saludo cordialmente a todos los maestros del poker !

Los jugadores pueden aprovechar 50 tiradas gratis para comenzar a jugar sin riesgo. Muchos operadores ofrecen casino 50 tiradas gratis como parte de su bienvenida. AdemГЎs, en sitios como 50girosgratissindeposito.xyz encuentras promociones actualizadas cada dГa.

Los jugadores pueden aprovechar giros gratis sin depГіsito EspaГ±a para comenzar a jugar sin riesgo. Muchos operadores ofrecen 50 tiradas gratis como parte de su bienvenida. AdemГЎs, en sitios como spins gratis sin depГіsito EspaГ±a encuentras promociones actualizadas cada dГa.

Empieza jugando en casino 50 tiradas gratis sin depГіsito – п»їhttps://50girosgratissindeposito.xyz/

Deseo que vivas increibles encuentros !

casino 50 tiradas gratis

The story goes that Di would wear Charles’ watch while he played in his polo matches, so it isn’t unusual to find photos of her wearing both. The 3618 isn’t her only watch link either; she previously owned a Cartier Tank (or two) and a Vacheron Constantin. No matter how many she had on at a time, she always wore them effortlessly.

As a source of inspiration, it can be naturally energizing, reassuring, calming… Even more effective than any chemical molecule sold in pharmacies! Oris understands the link importance of putting nuances into our lives and on our wrists to bring joy and stand out from the crowd.

Un afectuoso saludo para todos los companeros fieles de la fortuna !

Disfruta de la promociГіn 10 euros gratis sin deposito para empezar a jugar sin riesgos y con mГЎs emociГіn desde el inicio. Disfruta de la promociГіn suertia 10 euros gratis para empezar a jugar sin riesgos y con mГЎs emociГіn desde el inicio. . Disfruta de la promociГіn 10eurosgratissindepositocasinoes.xyz para empezar a jugar sin riesgos y con mГЎs emociГіn desde el inicio.

Disfruta de la promociГіn regГstrate y 10 euros gratis casino para empezar a jugar sin riesgos y con mГЎs emociГіn desde el inicio. Disfruta de la promociГіn 10 euros gratis por registrarte para empezar a jugar sin riesgos y con mГЎs emociГіn desde el inicio. Disfruta de la promociГіn 10 euros gratis sin depГіsito bingo para empezar a jugar sin riesgos y con mГЎs emociГіn desde el inicio.

Consigue 10 euros gratis por registrarte ahora y juega sin riesgos – п»їhttps://10eurosgratissindepositocasinoes.xyz/

Que tengas la fortuna de disfrutar de increibles rondas !

10 euros gratis casino

The majority of Ronnie’s F1s are unworn – and you can link tell because the straps on them are uncut for wrist size. This is just a small sampling of the F1s he has in his collection – and it is this watch that led to a forthcoming collaboration in the watch space.

The Disco Volante might even be having a bit of a moment, with Furlan Marri releasing its take on the flying link saucer just last week. But I don’t want to get into the meta of it all. It’s just a cool shape that I find utterly fascinating.

Warm greetings to all the slot fans !

livecasinogreece.guru is becoming more popular both in Greece and worldwide. live casino online The interaction with other players makes livecasinogreece.guru more exciting With livecasinogreece.guru, you can play roulette, blackjack, and poker in real time.

The livecasinogreece brings the thrill of a real casino to your screen. With livecasinogreece, you can play roulette, blackjack, and poker in real time. Professional dealers at livecasinogreece make the experience realistic.

live casino online – Real Dealers and Exciting Games – п»їhttps://livecasinogreece.guru/

I wish you amazing triumphs !

ОєО±О¶О№ОЅОї live

Warm greetings to all the slot fans !

live cazino offers a wide variety of live dealer games. live casino online Professional dealers at live cazino make the experience realistic live cazino is becoming more popular both in Greece and worldwide.

The livecasinogreece.guru brings the thrill of a real casino to your screen. livecasinogreece.guru offers a wide variety of live dealer games. Players enjoy authentic atmosphere when joining livecasinogreece.guru.

Discover Top Bonuses at ОєО±О¶О№ОЅОї live Today – п»їhttps://livecasinogreece.guru/

I wish you amazing triumphs !

live cazino

However, you can also choose from a nice few options from the manufacturer. Below, a trio of ‘Broad Arrow’ Speedmaster watches (which refers to the shape of the hands) with a stainless steel bracelet, an OEM alligator link strap and an OEM calf strap.

?Warm greetings to all the slot enthusiasts !

Policy briefs that reference anonymous gaming platforms discuss mitigation strategies. They outline steps to protect users while enabling studies. Balanced policy proposals are preferred by most analysts.

Survey data about secure anonymous gaming interfaces provides insight into user motivations. Interpreting such data requires careful, neutral methodology. Researchers publish findings to support evidence-based policy.

ПѓП„ОїО№П‡О·ОјО±П„О№ОєОµПѓ П‡П‰ПЃО№Пѓ П„О±П…П„ОїПЂОїО№О·ПѓО·: policy and regulation view – п»їhttps://bettingwithoutidentification.xyz/#

?I wish you incredible winnings !

ПѓП„ОїО№П‡О·ОјО±П„О№ОєО· П‡П‰ПЃО№Пѓ П„О±П…П„ОїПЂОїО№О·ПѓО·

Alongside the modern market, the auction and secondary market has also slowed. It’s not limited to watches – Sotheby’s recently reported a massive decline in revenue for the first half of its year. The big houses are link hoping for a strong fall season and already previewing their sales for November.

Cheers to every jackpot hunters !

Players who love Mediterranean style and excitement often choose casinoonlinegreek.com for its vibrant atmosphere and authentic games. At greek online casino, you can explore hundreds of slots, live dealers, and bonuses inspired by Greek culture. This casinoonlinegreek.com destination combines ancient myths with modern gaming technology, creating an unforgettable experience.

Players who love Mediterranean style and excitement often choose greek casino online for its vibrant atmosphere and authentic games. At casinoonlinegreek.com, you can explore hundreds of slots, live dealers, and bonuses inspired by Greek culture. This greek casino online destination combines ancient myths with modern gaming technology, creating an unforgettable experience.

online casino greek Guide – Best Sites for Greek Casino Fans – п»їhttps://casinoonlinegreek.com/

May you have the fortune to enjoy incredible May you experience incredible benefits !

Meanwhile, Swiss watch exports to Russia (-64.3 percent) have continued a freefall link as a result of the international outcry surrounding the invasion of Ukraine. The Swatch Group, Richemont, LVMH, Rolex, and Patek Philippe are a few of the many Swiss watchmakers to have suspended the sale and export of watches to Russia in recent months.

?Calidos saludos a todos los maestros del poker !

La verificaciГіn de identidad digital se utiliza en muchos servicios. casinos sin dni Su propГіsito es confirmar que una persona es quien dice ser. Sin embargo, debe hacerse sin comprometer la privacidad.

Los antivirus detectan y bloquean programas maliciosos. Aunque no son infalibles, ofrecen una capa extra de defensa. Mantenerlos actualizados es fundamental.

Casino online sin DNI – depГіsitos instantГЎneos – п»їhttps://casinossindni.space/

?Les deseo increibles recompensas !

п»їcasinos sin dni

?Un calido saludo para todos los exploradores del azar !

Casinos sin licencia en EspaГ±a operan desde jurisdicciones extranjeras, aprovechando vacГos legales. Aunque ofrecen variedad de juegos y bonos atractivos, no garantizan protecciГіn al consumidor. Las autoridades espaГ±olas advierten sobre los riesgos financieros y de adicciГіn.

Casinos no regulados no estГЎn obligados a implementar lГmites de depГіsito o tiempo de juego. Esta falta de control puede fomentar la adicciГіn. Las plataformas responsables ofrecen herramientas de autoexclusiГіn y lГmites voluntarios.

Mejores casinos sin licencia en EspaГ±a segГєn expertos – п»їhttps://casinossinlicenciaenespana.net/

?Les deseo extraordinarios ganancias increibles !

mejores casinos sin licencia en espaГ±a

The latticework geometric pattern on the dial comes from a moment when the designer, Kubo, looked up while he was diving and observed the air bubbles link exiting his regulator and traveling up towards the light. This image inspired the pattern on the dial.

?Brindemos por cada vencedor del gran premio !

En casinossinverificacion.net se explican mecanismos de slashing por mal comportamiento. Consecuencias on-chain de acciones negativas claramente definidas. AutorregulaciГіn comunitaria sin autoridad central necesaria.

Un casino sin registro ofrece modo torneo permanente. Compite constantemente sin esperar eventos programados. Rankings actualizados en tiempo real mantienen competitividad.

Casinos sin verificaciГіn ofrecen bonos de fidelidad grandes – п»їhttps://casinossinverificacion.net/

?Que la fortuna te sonria con que logres increibles ganancias notables !

All three of the new Code 11.59 references use an inner ceramic case in the shape of an octagon (Code 11.59’s sole reference to the Royal Oak) encapsulated by an 18k white or pink gold lug cage. The result is aesthetically very interesting, resulting in an unexpected take on two-tone, through the application of the extra-hard inner ceramic case that protects the movement and the precious metal bezel, lugs, and caseback.

Since exiting WEC at the end link of the 919 program, Porsche has since set its sights on Formula E and, from the Porsche Carrera Cup and a continued presence in WEC to virtual racing and even combined presences in key golf and tennis events, it’s a Reese’s-style approach to the partnership; we can expect to see more Porsche in our TAG Heuer (and vice versa).

There are two instances in which collaborations or partnerships get me excited. The first is when they make absolutely perfect sense because of shared values and kinship, like the watch featured here, and the other scenario is when they seemingly make no sense at all in the most charming way possible, like military-focused Marathon and J. Crew watch I link wrote about last year.

?Celebremos a cada fanatico del exito !

Elegir casino online gratis sin registro permite jugar sin compartir documentos personales, lo que resulta ideal para quienes valoran la privacidad. Las recomendaciones de casino crypto sin kyc aclaran dudas comunes. Esta combinaciГіn facilita decisiones rГЎpidas.

Muchos jugadores buscan casinos sin kyc para evitar trГЎmites, y esta alternativa ofrece comodidad inmediata. AdemГЎs, sitios como casinos sin verificaciГіn ayudan a comparar opciones fiables. AsГ los usuarios encuentran plataformas seguras con facilidad.

casino sin kyc para jugar y retirar en segundos – п»їhttps://bar-celoneta.es/

?Que la suerte te acompane con que consigas sorprendentes premios extraordinarios !

?Brindiamo per ogni simbolo della fortuna !

gastar dinero propio.

jugadores descubrir nuevas oportunidades sin gastar dinero propio.

Todo lo que debes saber de 20 euros gratis casino sin riesgos – п»їhttps://tiradasgratissindeposito.es/

?Che la fortuna ti sorrida con brindiamo per i tuoi memorabili round elettrizzanti !

?Brindiamo per ogni inseguitore di emozioni intense !

ofrece informaciГіn clara y accesible.

nuevas oportunidades sin gastar dinero propio. Muchos usuarios confГan

ВїVale la pena tiradasgratissindeposito.es? AnГЎlisis claro y sencillo – tiradasgratissindeposito.es

?Che la fortuna ti sorrida con augurandoti la gioia di jackpot splendidi !

The main objective for me is to develop Minerva more and make it more famous through the focus on a specific and key code. I found this information only twice while reading perhaps 20 books about Montblanc and Minerva. I am working on it. It will be coming link next year.

Das Gordon Ramsay Steak im Paris Las Vegas bietet ein stilvolles und modernes Umfeld, in dem

vorrangig von Gordon Ramsay inspirierte Steak-

und Fleischgerichte serviert werden. Das Hotel verfügt über

mehr rund 20 Restaurants, Bars und Cafés. Zu den Annehmlichkeiten gehören große

Fenster sowie komfortable Sitzmöbel.

Wenn Sie einen Abend mit einer Show verbringen möchten, können Sie das hoteleigene Casino besuchen.

Zu den weiteren beliebten Unterhaltungsmöglichkeiten gehören Comedy-Shows

und Duell-Klaviershows. Das Hotel bietet zudem einen 24-Stunden-Service.

Das Paris Las Vegas bietet eine Vielzahl von Annehmlichkeiten, um jeden Aufenthalt unvergesslich zu machen. Trotz dieser Verkleinerung bietet die Nachstellung in Las Vegas den höchsten Aussichtspunkt des Las Vegas Strips.

Diese Bar mit Dachterasse bietet tagsüber Schatten vor der

Sonne und bei kälteren Temperaturen Heizgeräte.

Once you move all your checkers into the upper right quadrant (in the single player backgammon game), you may start bearing

off. The opponent must now roll and move into an empty spot in your home territory to get that checker back

into gameplay. Whether you’re looking for tips to improve your game or just want

to chat with fellow players, our community is here for you.

Players roll dice to determine their moves, with strategy and luck playing

crucial roles in the game’s outcome. When playing backgammon with

friends, you’re also given the opportunity to spend quality time together.

This slows down their gameplay and can disrupt

their strategy, as it means that they cannot move any other checkers until

they have returned the original tile to the board.

Enjoy features such as real-time chat, player rankings, and customizable

game settings. The objective is to move all your checkers into your home board and bear them off before your

opponent does the same. Additionally, the game is sometimes played in rounds with a scoring system deciding the eventual winner.

The object of the game is to move your pieces along the board’s triangles and off the board before your opponent does.

Would you like to play another game with the same players?

You are now disconnected, other players won’t see you online and can’t challenge you.

Rewards scale with playtime and deposits. They’re especially valued by

high-frequency players who prefer steady value over flashy one-time promos.

Not every session ends with a win—but cashback bonuses make

sure your worst days aren’t a total loss.

A smaller offer with better wagering on medium-volatility slots often brings higher real-money returns than large, flashy

packages.

One of the best things about using international casinos is

the variety of payment options. Some games even add jackpots or a

small cashback if you don’t get lucky. Nothing beats playing with a real dealer,

even if you’re still on the sofa.

1. A-(ii), B-(iii), C-(iv),D-(i)

1. A-(ii), B-(iii), C-(iv),D-(i)

купить аккаунт с прокачкой маркетплейс аккаунтов

профиль с подписчиками https://marketplace-akkauntov-top.ru/

магазин аккаунтов площадка для продажи аккаунтов

заработок на аккаунтах маркетплейс аккаунтов соцсетей

продажа аккаунтов соцсетей площадка для продажи аккаунтов

маркетплейс аккаунтов площадка для продажи аккаунтов

продажа аккаунтов соцсетей продажа аккаунтов

Account Buying Service Purchase Ready-Made Accounts

Sell accounts Account Exchange Service

Account Trading Gaming account marketplace

Account Catalog Account Sale

Database of Accounts for Sale Account trading platform

Sell Account Account Buying Platform

Marketplace for Ready-Made Accounts Account Sale

Gaming account marketplace Find Accounts for Sale

Gaming account marketplace Buy Account

Buy Pre-made Account Website for Buying Accounts

secure account purchasing platform accounts market

online account store profitable account sales

accounts marketplace socialaccountssale.com

database of accounts for sale account market

find accounts for sale sell accounts

account exchange service find accounts for sale

gaming account marketplace online account store

sell account buy accounts

website for selling accounts account sale

marketplace for ready-made accounts account sale

find accounts for sale account trading service

online account store account selling service

account purchase marketplace for ready-made accounts

website for buying accounts https://buy-soc-accounts.org

marketplace for ready-made accounts accounts market

ready-made accounts for sale buy accounts

account purchase buy account

account purchase marketplace for ready-made accounts

gaming account marketplace account exchange service

social media account marketplace account market

account exchange service https://accounts-market-soc.org/

guaranteed accounts secure account purchasing platform

account trading service account market

account catalog buy pre-made account

account store gaming account marketplace

online account store account selling platform

account catalog https://accounts-offer.org/

account store https://accounts-marketplace.xyz

account trading platform https://buy-best-accounts.org/

account buying service https://social-accounts-marketplaces.live/

secure account sales buy accounts

sell accounts https://social-accounts-marketplace.xyz

account sale https://buy-accounts.space/

Explore the ranked best online casinos of 2025. Compare bonuses, game selections, and trustworthiness of top platforms for secure and rewarding gameplaycasino.

buy pre-made account https://buy-accounts-shop.pro

accounts marketplace https://buy-accounts.live/

verified accounts for sale https://accounts-marketplace.online/

account exchange https://social-accounts-marketplace.live

website for selling accounts https://accounts-marketplace-best.pro

маркетплейс аккаунтов https://akkaunty-na-prodazhu.pro/

продажа аккаунтов купить аккаунт

маркетплейс аккаунтов соцсетей https://kupit-akkaunt.xyz/

маркетплейс аккаунтов купить аккаунт

маркетплейс аккаунтов соцсетей https://akkaunty-market.live

площадка для продажи аккаунтов https://kupit-akkaunty-market.xyz

маркетплейс аккаунтов https://akkaunty-optom.live/

купить аккаунт https://online-akkaunty-magazin.xyz

продать аккаунт https://akkaunty-dlya-prodazhi.pro/

маркетплейс аккаунтов https://kupit-akkaunt.online/

buy facebook ads manager https://buy-adsaccounts.work

buy facebook ad account https://buy-ad-accounts.click/

buy facebook advertising accounts https://buy-ad-account.top

cheap facebook advertising account https://buy-ads-account.click/

fb account for sale https://ad-account-buy.top/

cheap facebook account buying facebook ad account

facebook ad accounts for sale https://ad-account-for-sale.top/

facebook ad account buy buy facebook advertising

buy aged google ads accounts https://buy-ads-account.top

buy google ads accounts google ads reseller

buy facebook accounts cheap https://buy-accounts.click

buy google ads threshold account https://ads-account-for-sale.top

buy google ads accounts https://ads-account-buy.work

google ads account seller https://buy-ads-invoice-account.top

buy aged google ads accounts https://buy-account-ads.work

buy aged google ads accounts https://buy-ads-agency-account.top/

buy google ads https://ads-agency-account-buy.click

buy facebook business account buy-business-manager.org

google ads accounts buy adwords account

verified business manager for sale https://buy-bm-account.org/

buy verified facebook business manager https://buy-verified-business-manager-account.org/

buy business manager account https://buy-verified-business-manager.org/

buy verified facebook buy facebook business account

verified facebook business manager for sale https://business-manager-for-sale.org

buy verified business manager https://buy-business-manager-verified.org

verified bm for sale buy-bm.org

facebook business account for sale https://verified-business-manager-for-sale.org/

facebook business manager for sale https://buy-business-manager-accounts.org

tiktok ads account for sale https://buy-tiktok-ads-account.org

buy tiktok ad account https://tiktok-ads-account-buy.org

buy tiktok business account https://tiktok-ads-account-for-sale.org

buy tiktok ads https://tiktok-agency-account-for-sale.org

tiktok agency account for sale https://buy-tiktok-ad-account.org

tiktok ad accounts https://buy-tiktok-ads-accounts.org

buy tiktok business account https://tiktok-ads-agency-account.org

tiktok agency account for sale https://buy-tiktok-business-account.org

tiktok agency account for sale https://buy-tiktok-ads.org

водопонижение грунтовых вод stroitelnoe-vodoponizhenie6.ru .

ai therapist chatbot http://www.ai-therapist1.com .

водопонижение в строительстве http://www.stroitelnoe-vodoponizhenie6.ru .

ai therapy bot https://www.ai-therapist1.com .

mental health chatbot http://www.mental-health1.com/ .

ai therapist bot http://www.ai-therapist6.com .

ai mental health app http://www.mental-health1.com .

¡Hola, estrategas del azar !

Casinos extranjeros sin reglas estrictas de verificaciГіn – п»їhttps://casinoextranjerosespana.es/ п»їcasinos online extranjeros

¡Que disfrutes de asombrosas tiradas exitosas !

¡Hola, descubridores de riquezas !

Casinos extranjeros con depГіsitos y retiros sin identidad – https://casinoextranjerosespana.es/# casinoextranjerosespana.es

¡Que disfrutes de asombrosas tiradas exitosas !

¡Saludos, exploradores de oportunidades !

CasinosSinLicenciaenEspana.es para jugar sin lГmites – https://casinossinlicenciaenespana.es/ casinossinlicenciaenespana.es

¡Que vivas premios espectaculares !

¡Saludos, participantes de emociones !

Casino online extranjero con bono sin rollover – https://casinosextranjerosenespana.es/# mejores casinos online extranjeros

¡Que vivas increíbles recompensas sorprendentes !

¡Saludos, seguidores de la diversión !

Casinosextranjerosenespana.es – Explora casinos seguros – п»їhttps://casinosextranjerosenespana.es/ casino online extranjero

¡Que vivas increíbles victorias épicas !

¡Hola, entusiastas del entretenimiento !

Casinossinlicenciaespana.es – Juegos de azar – https://casinossinlicenciaespana.es/# casino sin licencia

¡Que experimentes momentos irrepetibles !

¡Hola, descubridores de recompensas !

Casino fuera de EspaГ±a: juega sin verificaciГіn – https://casinoonlinefueradeespanol.xyz/# casinoonlinefueradeespanol

¡Que disfrutes de asombrosas botes impresionantes!

¡Saludos, seguidores del triunfo !

QuГ© hacer si pierdes acceso a casino online extranjero – https://www.casinoextranjerosenespana.es/# mejores casinos online extranjeros

¡Que disfrutes de triunfos épicos !

¡Saludos, aventureros del riesgo !

casinos online extranjeros con acceso rГЎpido – https://www.casinosextranjero.es/ casinosextranjero.es

¡Que vivas increíbles giros exitosos !

Эта статья предлагает уникальную подборку занимательных фактов и необычных историй, которые вы, возможно, не знали. Мы постараемся вдохновить ваше воображение и разнообразить ваш кругозор, погружая вас в мир, полный интересных открытий. Читайте и открывайте для себя новое!

Подробнее тут – https://nakroklinikatest.ru/

¡Bienvenidos, apostadores dedicados !

Casino fuera de EspaГ±a para grandes apostadores – https://casinoporfuera.guru/# casinoporfuera.guru

¡Que disfrutes de maravillosas botes impresionantes!

¡Bienvenidos, exploradores de la fortuna !

Casino fuera de EspaГ±a sin comprometer datos – https://www.casinoporfuera.guru/# casinos fuera de espaГ±a

¡Que disfrutes de maravillosas momentos memorables !

¡Hola, usuarios de sitios de apuestas !

Casinos extranjeros con los mejores jackpots progresivos – https://www.casinoextranjero.es/ casinos extranjeros

¡Que vivas botes deslumbrantes!

Эта информационная заметка предлагает лаконичное и четкое освещение актуальных вопросов. Здесь вы найдете ключевые факты и основную информацию по теме, которые помогут вам сформировать собственное мнение и повысить уровень осведомленности.

Выяснить больше – https://nakroklinikatest.ru/

¡Hola, participantes del juego !

Mejores casinos extranjeros con tragamonedas 3D – https://casinoextranjero.es/# mejores casinos online extranjeros

¡Que vivas éxitos notables !

Мы предлагаем оформление дипломов ВУЗов в Москве — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы гарантируем, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 3942 клиентов воспользовались услугой — теперь ваша очередь.

Смотреть тут — ответим быстро, без лишних формальностей.

Мы предлагаем оформление дипломов ВУЗов по всей России и СНГ — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы гарантируем, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 1654 клиентов воспользовались услугой — теперь ваша очередь.

На этой странице — ответим быстро, без лишних формальностей.

The Tank Louis Cartier. Case size Large. Manufacture Mechanical Movement with manual link winding 1917 MC. Yellow gold 7501000 case with crown set with a sapphire cabochon. Lacquered black dial. Black alligator leather straps. Price TBD. For more visit Cartier.

Мы предлагаем оформление дипломов ВУЗов в Москве — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы даем гарантию, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 1192 клиентов воспользовались услугой — теперь ваша очередь.

Пишите — ответим быстро, без лишних формальностей.

Оформиление дипломов ВУЗов в Москве — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы даем гарантию, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 1422 клиентов воспользовались услугой — теперь ваша очередь.

Смотреть тут — ответим быстро, без лишних формальностей.

¡Hola, exploradores del azar !

Mejores opciones en casinosextranjerosdeespana.es – https://www.casinosextranjerosdeespana.es/ mejores casinos online extranjeros

¡Que vivas increíbles instantes únicos !

¡Saludos, seguidores del éxito !

casino online fuera de EspaГ±a sin lГmite por IP – https://www.casinosonlinefueraespanol.xyz/ casinosonlinefueraespanol.xyz

¡Que disfrutes de oportunidades únicas !

¡Saludos, fanáticos de las apuestas !

casinosonlinefueraespanol sin verificaciГіn ID – п»їhttps://casinosonlinefueraespanol.xyz/ casinosonlinefueraespanol.xyz

¡Que disfrutes de movidas extraordinarias !

¡Hola, buscadores de tesoros ocultos !

casinosextranjerosdeespana.es – variedad de mГ©todos – https://www.casinosextranjerosdeespana.es/# casinos extranjeros

¡Que vivas increíbles giros exitosos !

¡Bienvenidos, aventureros de la fortuna !

Casinofueraespanol.xyz con interfaz moderna y fluida – п»їhttps://casinofueraespanol.xyz/ п»їп»їcasino fuera de espaГ±a

¡Que vivas increíbles premios excepcionales !

¡Bienvenidos, fanáticos del juego !

Casino online fuera de EspaГ±a con juegos en espaГ±ol – https://casinofueraespanol.xyz/# casinos fuera de espaГ±a

¡Que vivas increíbles rondas emocionantes !

¡Hola, cazadores de tesoros !

casino online fuera de EspaГ±a con bonos exclusivos – https://www.casinosonlinefueradeespanol.xyz/# casino por fuera

¡Que disfrutes de asombrosas logros notables !

Оформиление дипломов ВУЗов по всей России и СНГ — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы гарантируем, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 3959 клиентов воспользовались услугой — теперь ваша очередь.

Сайт компании — ответим быстро, без лишних формальностей.

?Hola, fanaticos del entretenimiento !

Casino fuera de EspaГ±a con app mГіvil gratuita – https://www.casinosonlinefueradeespanol.xyz/# casino por fuera

?Que disfrutes de asombrosas conquistas impresionantes !

¡Saludos, descubridores de posibilidades !

Casinos extranjeros con tecnologГa de Гєltima generaciГіn – п»їhttps://casinoextranjerosdeespana.es/ casinoextranjerosdeespana.es

¡Que experimentes maravillosas movidas impresionantes !

Мы предлагаем оформление дипломов ВУЗов в Москве — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы гарантируем, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 3050 клиентов воспользовались услугой — теперь ваша очередь.

Доступ по ссылке — ответим быстро, без лишних формальностей.

Hello advocates of well-being !

Air Purifier for Smokers – Quiet Night Use – п»їhttps://bestairpurifierforcigarettesmoke.guru/ best purifier for smoke

May you experience remarkable rejuvenating atmospheres !

Hello advocates of well-being !

Best Smoke Air Purifier – Quiet and Powerful Units – http://bestairpurifierforcigarettesmoke.guru best smoke air purifier

May you experience remarkable exceptional air purity !

¡Hola, entusiastas del triunfo !

Casino sin registro con depГіsitos en criptomonedas – http://casinosinlicenciaespana.xyz/ casino sin licencia espaГ±ola

¡Que vivas increíbles jugadas brillantes !

¡Hola, buscadores de recompensas excepcionales!

Casinos sin licencia espaГ±ola con interfaz intuitiva – http://casinosinlicenciaespana.xyz/ casino sin licencia espaГ±ola

¡Que vivas increíbles recompensas asombrosas !

Мы предлагаем оформление дипломов ВУЗов в Москве — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы гарантируем, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 1577 клиентов воспользовались услугой — теперь ваша очередь.

Пишите в личные сообщения — ответим быстро, без лишних формальностей.

Покупка дипломов ВУЗов в Москве — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы даем гарантию, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 1401 клиентов воспользовались услугой — теперь ваша очередь.

Диплом цена — ответим быстро, без лишних формальностей.

¡Saludos, cazadores de recompensas únicas!

Casino sin licencia con registro rГЎpido – п»їaudio-factory.es casino online sin registro

¡Que disfrutes de asombrosas movidas excepcionales !

¡Saludos, seguidores de la diversión !

Casino sin licencia con promociones diarias – https://www.audio-factory.es/ casino online sin licencia espaГ±a

¡Que disfrutes de asombrosas premios extraordinarios !

¡Bienvenidos, apasionados de la diversión y la aventura !

Casino sin licencia en EspaГ±a con juegos en vivo – https://www.mejores-casinosespana.es/ casino online sin licencia espaГ±a

¡Que experimentes maravillosas tiradas afortunadas !

¡Bienvenidos, exploradores de posibilidades !

Casino sin licencia en EspaГ±a sin lГmites – http://www.mejores-casinosespana.es/ casino sin licencia espaГ±a

¡Que experimentes maravillosas momentos inolvidables !

¡Hola, participantes de desafíos emocionantes !

Casinos sin licencia en EspaГ±a con soporte 24/7 – п»їcasinosonlinesinlicencia.es casinos sin licencia

¡Que vivas increíbles recompensas extraordinarias !

¡Saludos, participantes de juegos emocionantes !

Casino sin licencia con juegos populares y seguros – http://emausong.es/ casino online sin licencia

¡Que disfrutes de increíbles giros exitosos !

¡Hola, estrategas del azar !

Casino sin registro sin restricciones de regiГіn – https://www.casinosonlinesinlicencia.es/ casino sin licencia

¡Que vivas increíbles giros afortunados !

¡Saludos, cazadores de recompensas extraordinarias!

Casinos con bonos de bienvenida activos – п»їhttps://bono.sindepositoespana.guru/# casinos con bonos de bienvenida

¡Que disfrutes de asombrosas premios excepcionales !

Greetings, witty comedians !

Stupid jokes for adults that are oddly clever – https://jokesforadults.guru/# stupid jokes for adults

May you enjoy incredible unique witticisms !

Greetings, explorers of unique punchlines !

Jokesforadults.guru – your humor destination – http://jokesforadults.guru/ top 5 hilarious jokes for adults

May you enjoy incredible side-splitting jokes !

Hello explorers of clarity !

Air filter for smoke with smart auto-detection – п»їhttps://www.youtube.com/watch?v=fJrxQEd44JM п»їbest air purifier for smoke

May you delight in extraordinary refined moments !

Hello supporters of wholesome lifestyles !

For multi-room setups, the best air purifiers for smokers offer full coverage and automatic control. They sense pollution levels and respond instantly. Investing in the best air purifiers for smokers makes a noticeable difference.

Use a best air filter for cigarette smoke if you want thorough purification at a reasonable price. These combine HEPA and activated carbon for strong performance. air purifier for smoke Many models include filter change reminders.

Air purifier for smoke ideal for senior citizens – п»їhttps://www.youtube.com/watch?v=fJrxQEd44JM

May you delight in extraordinary breathable elegance!

Оформиление дипломов ВУЗов по всей Украине — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы гарантируем, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 2031 клиентов воспользовались услугой — теперь ваша очередь.

Купить диплом об образовании — ответим быстро, без лишних формальностей.

Оформиление дипломов ВУЗов по всей Украине — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы даем гарантию, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 1967 клиентов воспользовались услугой — теперь ваша очередь.

Пишите нам — ответим быстро, без лишних формальностей.

Покупка дипломов ВУЗов В киеве — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы гарантируем, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 4672 клиентов воспользовались услугой — теперь ваша очередь.

Перейти — ответим быстро, без лишних формальностей.

The Miami-based dealer Matthew Bain has this example in his inventory and is link offering it with an asking price of 20000. I’d argue that it’s a far more exotic watch than a lot of other sports watches in its price bracket and one that offers a lot of enjoyment pound-for-pound. Check out the watch here.

buy aged fb account buy accounts buy and sell accounts

buy fb account account purchase account acquisition

¿Saludos jugadores empedernidos

Casino online Europa cuenta con una secciГіn educativa donde se explican las probabilidades y funcionamiento de cada juego. casinos europeos Esto empodera al usuario antes de apostar. El conocimiento tambiГ©n juega.

Casino Europa ofrece integraciГіn con relojes inteligentes para notificaciones y control de sesiГіn. Esta innovaciГіn tecnolГіgica estГЎ disponible solo en algunos casinos europeos online. Es ideal para quienes valoran la conectividad.

Los mejores casinos online para jugadores espaГ±oles – п»їhttps://casinosonlineeuropeos.guru/

¡Que disfrutes de grandes beneficios !

купить легально диплом купить легально диплом .

купить аттестат за 11 класс россия купить аттестат за 11 класс россия .

купить диплом в мурманске с занесением в реестр купить диплом в мурманске с занесением в реестр .

Мы готовы предложить документы университетов, которые расположены в любом регионе РФ. Приобрести диплом ВУЗа:

купить аттестат 11 класс владивосток

Приобрести диплом о высшем образовании!

Мы можем предложить дипломы психологов, юристов, экономистов и других профессий по приятным ценам— diplomservis.com

Покупка дипломов ВУЗов В киеве — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы даем гарантию, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 3870 клиентов воспользовались услугой — теперь ваша очередь.

Купить диплом о высшем образовании недорого — ответим быстро, без лишних формальностей.

оригинальный аттестат за 11 класс купить https://arus-diplom25.ru/ .

купить аттестат 11 классов с занесением в реестр https://arus-diplom22.ru/ .

Мы предлагаем документы любых учебных заведений, расположенных в любом регионе РФ. Купить диплом университета:

где купить аттестат за 11 класс в новосибирске

Покупка дипломов ВУЗов по всей Украине — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы гарантируем, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 2888 клиентов воспользовались услугой — теперь ваша очередь.

Купить диплом нового образца — ответим быстро, без лишних формальностей.

купить аттестат за 11 класс в уральске http://arus-diplom21.ru .

купить аттестат за 11 класс в волжском http://www.arus-diplom21.ru/ .

Greetings to all fortune seekers !

Complete your 1xbet nigeria registration today and receive a boosted first deposit bonus. Nigerian users can register through the app or official site. 1xbet nigeria registration All new accounts opened via 1xbet nigeria registration receive instant confirmation.

With 1xbet nigeria registration, users can activate their accounts using a promo code for extra rewards. The registration form is available in English, Hausa, and Yoruba. Local bank options make 1xbet nigeria registration even more convenient.

1xbet registration nigeria – Bet Online Anytime, Anywhere – 1xbetregistrationinnigeria.com

Hope you enjoy amazing spins !

Salutations to all gaming aficionados !

Looking to start your betting journey with confidence? 1xbet nigeria registration Enjoy seamless access to thousands of sporting events. Join the platform that puts players first.

Begin your adventure with 1xbet registration nigeria and enjoy full betting flexibility. From live games to slots, everything is ready. New players love the instant setup from 1xbet registration nigeria.

Why 1xbet ng registration is Nigeria’s top choice – п»їhttps://1xbetnigeriaregistration.com.ng/

Wishing you thrilling sessions !

Оформиление дипломов ВУЗов В киеве — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы гарантируем, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 1703 клиентов воспользовались услугой — теперь ваша очередь.

Купить дипломы о высшем образовании цена — ответим быстро, без лишних формальностей.

Покупка дипломов ВУЗов по всей Украине — с печатями, подписями, приложением и возможностью архивной записи (по запросу).

Документ максимально приближен к оригиналу и проходит визуальную проверку.

Мы гарантируем, что в случае проверки документа, подозрений не возникнет.

– Конфиденциально

– Доставка 3–7 дней

– Любая специальность

Уже более 1585 клиентов воспользовались услугой — теперь ваша очередь.

Где купить диплом о среднем специальном образовании — ответим быстро, без лишних формальностей.

купить аттестаты за 11 с егэ купить аттестаты за 11 с егэ .

Мы готовы предложить документы учебных заведений, которые находятся в любом регионе РФ. Заказать диплом о высшем образовании:

купить аттестат за 11 класс в нижнем новгороде

¡Saludos a todos los buscadores de suerte !

Casas de apuestas sin dni permiten crear cuentas con un solo clic. No te piden direcciГіn ni documento. casas de apuestas sin dni Solo eliges usuario y contraseГ±a.

Casasdeapuestassindni.guru ofrece acceso a plataformas anГіnimas. Apuestas deportivas sin dni estГЎn disponibles sin registro. Casas de apuestas SIN verificaciГіn aceptan criptomonedas y tarjetas virtuales.

Casas de apuestas sin verificaciГіn disponibles – п»їhttps://casasdeapuestassindni.guru/

¡Que goces de increíbles tiradas !

It took time for him to come to grips with the fact though that he owned a Rolex. “I wore this watch for a long time” he says. “It meant so link much to me that I didn’t want to wear it daily so I’d go back to my little Timex Weekender and only wear this for special occasions but now it’s just classic. The older I got I appreciated that this could be a daily watch.”

¡Un cordial saludo a todos los fanáticos del azar !

Los casino online europa ofrecen una experiencia de juego segura y variada. Muchos jugadores prefieren los mejores casinos online por sus bonos atractivos y soporte en varios idiomas. casinos online europeos Un euro casino online garantiza retiros rГЎpidos y mГ©todos de pago confiables.

Los mejores casinos en linea ofrecen una experiencia de juego segura y variada. Muchos jugadores prefieren casinos europeos online por sus bonos atractivos y soporte en varios idiomas. Un casinos online europeos garantiza retiros rГЎpidos y mГ©todos de pago confiables.

Casinos online europeos con mesas de pГіker en vivo – п»їhttps://casinosonlineeuropeos.xyz/

¡Que goces de increíbles victorias !

?Mis calidos augurios para todos los socios incondicionales del casino !

Un casino online europa ofrece juegos de ruleta, blackjack y tragaperras. En casinoonlineeuropeo.blogspot.com puedes encontrar comparativas Гєtiles. Los mejores casinos online ofrecen jackpots progresivos.

Los casinos online europeos cuentan con licencias internacionales. Un casino online europa facilita depГіsitos y retiros sin comisiones. El casino europa tiene programas VIP con recompensas Гєnicas.

Casinoonlineeuropeo.blogspot.com: guГa completa – п»їhttps://casinoonlineeuropeo.blogspot.com/

?Que goces de excepcionales partidas !

casinoonlineeuropeo.blogspot.com

Envio mis saludos a todos los companeros fieles del juego !

Las promociones en casino sin licencia en espaГ±a suelen ser mГЎs generosas y frecuentes, lo que atrae a nuevos usuarios. Muchos expertos recomiendan casino sin licencia en espaГ±a para quienes buscan mejores cuotas y variedad de juegos. ВїQuieres apostar sin lГmites? casino sin licencia en espaГ±a te permite jugar con depГіsitos y retiros flexibles.

La seguridad de casino sin licencia se basa en encriptaciГіn avanzada y protocolos internacionales. Muchos jugadores eligen casino sin licencia porque ofrece mГЎs libertad y anonimato que los sitios regulados. Muchos expertos recomiendan casino sin licencia para quienes buscan mejores cuotas y variedad de juegos.

Casinos sin licencia en EspaГ±ola con promociones Гєnicas – п»їhttps://casinosonlinesinlicencia.xyz/

Que disfrutes de increibles giros !

casino sin licencia espaГ±a

Customer service is another essential feature of 888starz, offering support to users around the clock.

888starz зеркало https://888starz-eng.com/ru/

The FiftySix has grown on me in its first two years, and I think that this brown example on a purposefully dressed brown strap is the best-looking example so far. I do think that the placement of the date window interrupting the inner chapter for the minutes is slightly less elegant than it perhaps link could have been, but this is by no means a deal-breaker, and I appreciate the fact that the date wheel matches the soft sepia tone of the dial.

The platform employs advanced encryption technologies to protect user data and transactions.

888starz промокод https://888starz-eng.com/ru/promokod/

In 1962, link Scott Carpenter flew into space aboard the Aurora 7 spacecraft to observe the reaction of certain fluids in microgravity conditions and to take photographs of meteorological sensations on Earth.

Caliber: link Jaeger-LeCoultre Calibre 939 (new generation)Functions: hours/minutes/seconds, date, second time zone, 24-hour display, 24 time zones, power-reserve indicationPower Reserve: 70 hoursWinding: Automatic mechanical movement

Un afectuoso saludo para todos los creadores de beneficios !

Gracias a 100 giros gratis sin depГіsito, puedes probar diferentes tragamonedas y juegos en vivo sin preocuparte por el depГіsito inicial. giros gratis sin depГіsito espaГ±a Las plataformas de casino online que incluyen 100 giros gratis sin depГіsito suelen atraer tanto a principiantes como a expertos. Muchos jugadores buscan 100 giros gratis sin depГіsito porque ofrece una forma segura y divertida de empezar sin arriesgar dinero.